This post talks about the best bank for digital nomads! When traveling abroad, the financial planning portion can always be somewhat of a headache. Exchange rates and foreign transaction fees are just the beginning. As a digital nomad, what you have to consider can become even more confusing.

Some of the countries you may visit will have different transaction tendencies than you’re accustomed too. For example, when I arrived in India, I had an exceptionally challenging time finding ATMs. Many of the places I went to in Rishikesh didn’t accept cards. Do you see the predicament? Once, I found myself short of cash at one of the restaurants. The owner of the restaurant just told me to come back the next day and not to worry about it. At first, I was incredibly embarrassed. Then I thought about what this interaction would have been like at home. In America, an IOU would not have even been considered as an option. I share this with you to save you from potential hassle. The inconvenience and/or the embarrassment of not having money on hand can be an unnecessary stress.

If paying others is not something that concerns you, perhaps being paid is. You are working remotely. You could have clients in your home country or throughout the world. If the latter is applicable to you, you’ll want to put currency exchange fee at the top of your “must-have” list. Even if your clients are located in your home country, you will want to ensure that you select an institution that is reliable. Making sure that you get paid is important. Making sure that you get paid with ease and with as much of the original amount of money is ideal. Where that money goes is also vital. You’ll want to make sure that you choose a financial institution that best serves you.

Best Bank for Digital Nomads (Digital Nomad Banking Solutions)

Now that you understand why it is important to select a financial institution carefully. You will want to make a list of what you want it to do. To help you get started, here is a preliminary selection of topics to consider:

Foreign Transaction Fees – What are the institution’s fees for using your card in countries besides your own? These fees can vary and can add up quickly if you use your card frequently.

Exchange Rate Fees – Some institutions charge fees on top of the exchange rates. Other banks, like Revolut, only charge additional fees on the weekends or for specific types of currency.

Accessibility – Can you use your debit card in any foreign ATM or are you limited to only major foreign banking institutions? If you plan on exclusively using your credit card, do you need to have a pin number for it? This last question is one from experience. Years ago, I was traveling in Holland and I intended on only using my credit card. I overlooked the necessity of having a pin code to use for certain types of payment kiosks. I later learned that I’d tossed the pin code out because it was included in the fine print that came with the credit card. This was a nightmare. The credit card company’s policy refused my ability to received the pin code over the phone or by email. The benefit of this experience is that I can share my hard-earned lesson with you.

Card Management – What happens if your bank suspects fraud and freezes your card? Or, what happens if your card goes missing? What is their policy for replacing the card if you’re overseas? What is their expected delivery time? During this same trip that I previously mentioned, the person I was traveling with lost their credit card in the first few days as well. His credit card company did not have a quick overseas delivery time.

Income – As a digital nomad, you are working hard for the money. Being able to receive that money with ease is essential. Also, receiving as much of that money by avoiding currency or processing fees is ideal.

Customer Service – Does the company provide 24/7 customer service? How do they communicate? If they require a phone call exclusively and you are without the ability to use your phone, that could be a problem.

Peace of Mind – Is the bank insured by a larger governing body or do they have any guarantee that should their business go under you will not lose your money?

With all of these in mind, let’s take a look at some of the options the digital nomad banker has.

Transferwise

Pros: Transferwise claims itself to provide, “borderless accounts.” Its intention is to simplify money transferring and avoid high currency transfer fees. They are not an actual bank, which means you can’t get a line of credit with them, nor can you receive overdraft fees. These accounts accept 40 different currencies. This allows you to receive payments from all over the world. You can use it similarly to a bank account if you are a resident of the EU by getting a debit card. It is free to open an account. Any of the fees they do have are easily accessible to read about, meaning nothing is hidden.

Cons: If you’re not a resident of the EU, you can’t use the debit card. Also, if you’re moving locations frequently and consequently changing your sim card often, you may find it difficult to access your account due to their security measures associated with your cell phone number. Additionally, if you work with many international companies you may want to see what the primary currency you work with is. 40 currencies is a lot, but there are over 150 currencies in the world.

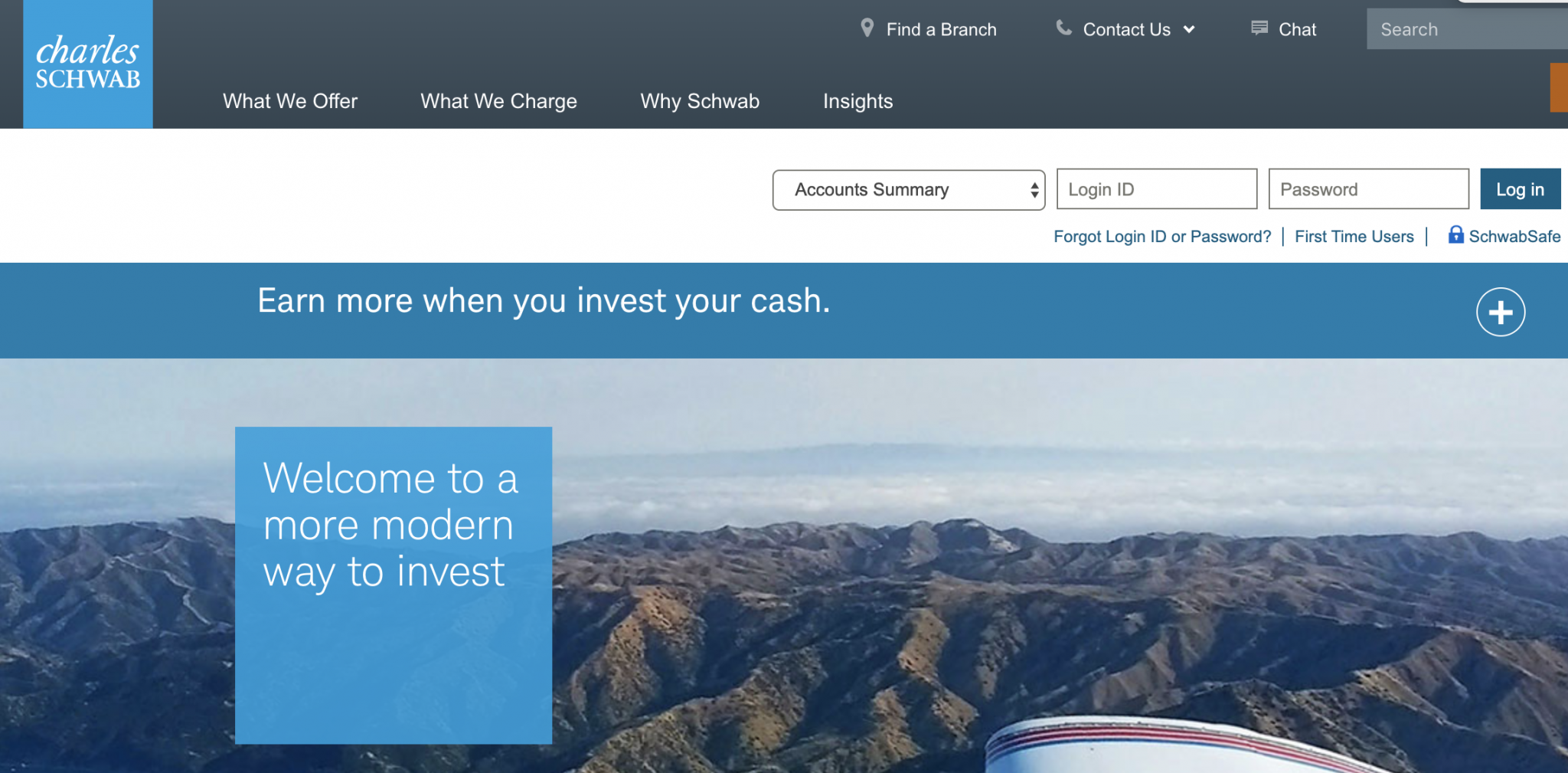

Charles Schwab

Pros: Charles Schwab is spectacular with regard to foreign transactions. They do not charge fees for debit card usage on ATMS, POS, or online usages domestically or abroad. Additionally, should you misplace your card, they are able to overnight the card to you for a fee.

Cons: Charles Schwab accounts are limited to US residents with an address, social security number, and state ID card or driver’s license. Additionally, when opening an account, they do a hard inquiry on your credit score.

Paypal

Pros: Paypal is kind of like old reliable. At one time, it was a bright new and shiny thing. Now, it’s just a tool that everyone has because it has been around long enough that everyone knows how to use it. The real upside to old reliable is Paypal Business. This service offers a flat fee of .50 for any payment amount. That is significant when you think about how percentage fees can add up.

Cons: If you’re not using the Business option, the payment options have a 2.9% fee with an additional .30 fee per transaction. If you’re doing business with a paypal account that is not from the same country as yours, the fee jumps to 3.9%. Also, if you forget to change your phone number for the account, you will lose access to it. I’m speaking from experience on this one.

N26

Pros: N26 is a mobile bank based out of Berlin, Germany. Their accounts come with a physical debit card (Mastercard), that can be used at any ATM to withdraw cash. They also offer cash withdrawals with CASH 26. This service allows you to show a barcode to any of the 15,000 participating shops in Austria or Germany to withdraw up to 200 euros in cash. It works with Google Pay and Apple Pay, and they work with Transferwise for currency exchanges. You also do not need to be a registered citizen to have an N26 account, only an address.

Cons: N26 is for the EU only. Other negative feedback includes very slow response times with their customer service support and glitches with their app.

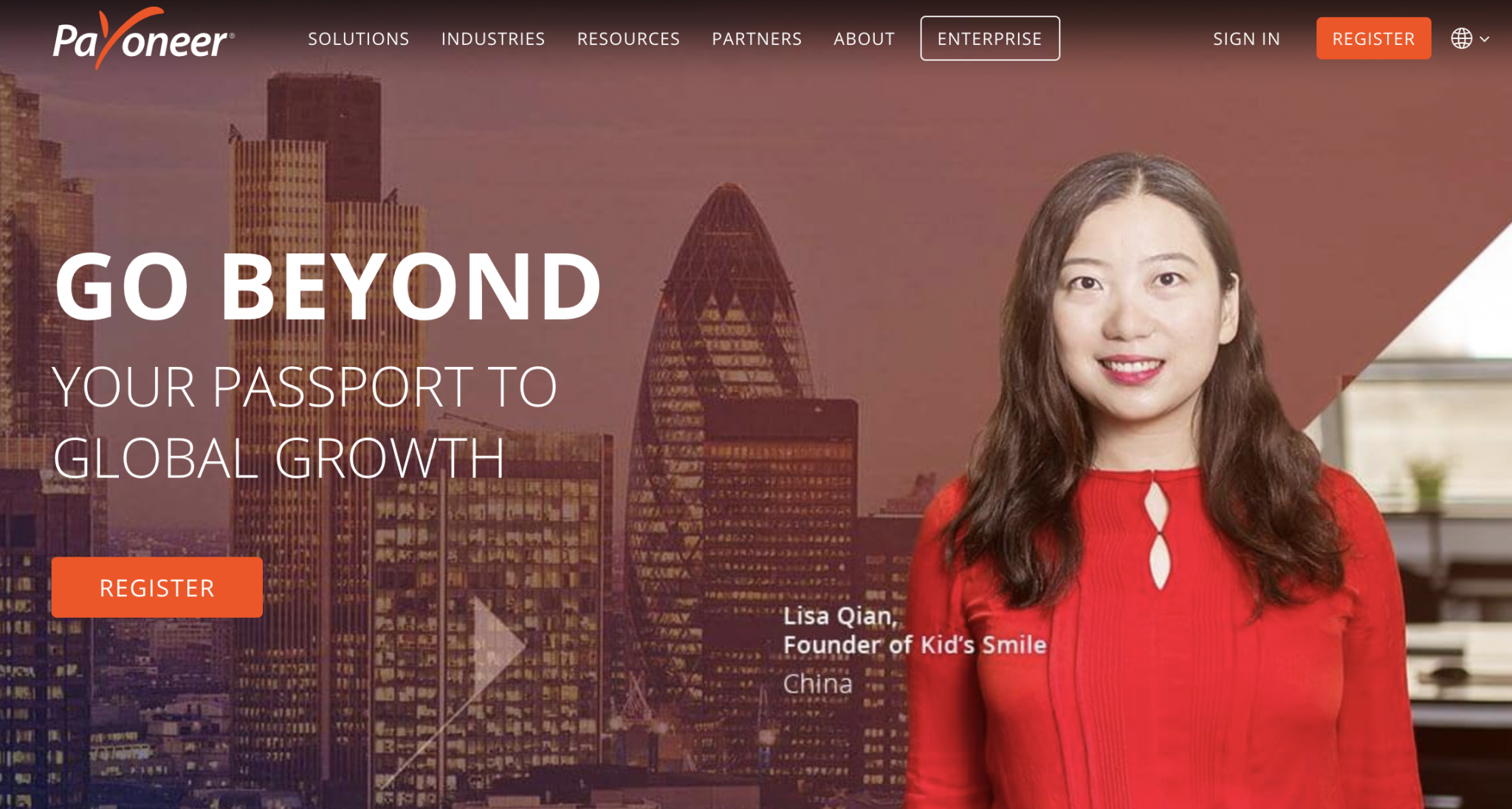

Payoneer

Pros: Payoneer is an online service provider that allows you to send and receive payments internationally between businesses and marketplaces. It is available in over 200 countries with an ability to process payments in 150 currencies. They have exceptionally high reviews for their customer service. They also offer a variety of options for sending and receiving payments. This allows you to cater their services according to your preferences.

Cons: This service is intended exclusively for business payments, receipts, and currency conversions. If you’re sending money for personal reasons, this option is not for you. There are also a variety of fees that can accumulate quickly.

Monese:

Pros: Monese is not a bank but an e-money firm. What does this mean? Monese does not reinvest funds. Customer funds are kept in a separate account that is inaccessible to Monese making 100% of customer funds protected, even if they go out of business. For the European nomad, Monese is a great option. You’re able to contact with their Customer service through chatbot, phone, or email.

Cons: Customer service is not available 24/7. If you’re in a pinch, you may have to be resourceful until you are able to connect with them. They also do not have a banking license which means there are no deposit guarantees. Additionally, they have a cap on how much you can withdraw or spend.

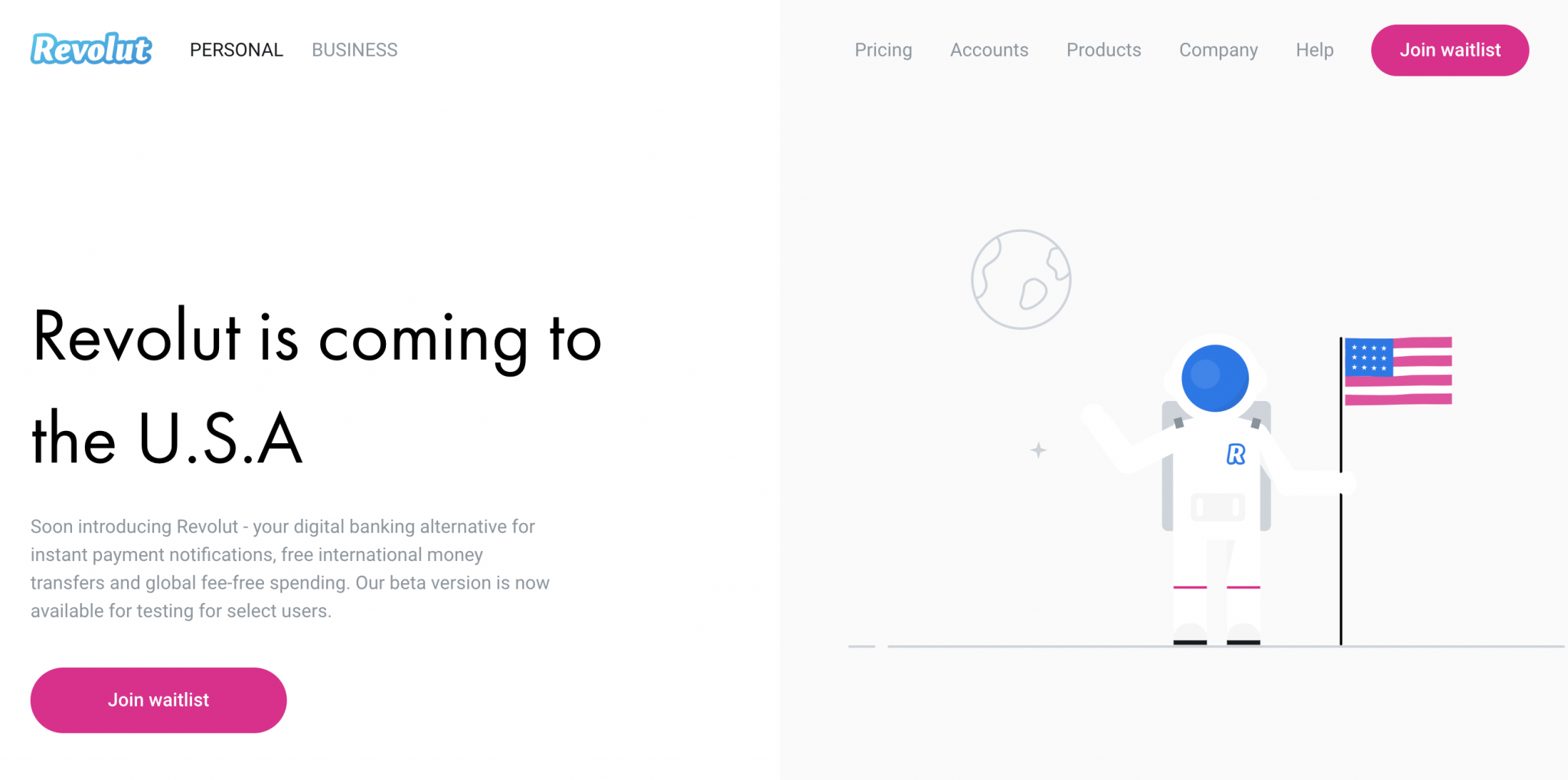

Revolut

Pros: Revolut is an online banking system that is based out of the UK. It has, by far, the highest reviews of any online banking institution that I have found. Good news for those of us who are not residents of the UK: Revolut supports legal residents of the following countries: United States, Canada, Singapore, Switzerland, Australia, Austria, Belgium, Bulgaria, Croatia, Republic of Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Latvia, Liechtenstein, Lithuania, Luxembourg, Malta, Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, all in addition to the United Kingdom.

They offer three different types of personal banking, one for every budget (including a free-ninety-nine option). They offer a relatively transparent foreign exchange rate interbank exchange rate. Monday – Friday there is no mark-up. However, on the weekends there is an additional percentage. They also have an additional fee for the Thai Baht and the Ukranian Hyrvania. They also offer free ATM withdrawals for up to £200 for their standard account level. Revolut not only offers Personal banking but Business banking as well. For those Digital Nomads that are freelancing, this is a great tool to use not to mix business and personal finances. They also offer a variety of travel insurance. If travel insurance is on your list, and it should be if it isn’t already, I recommend looking into it. Especially if you are the type of person who likes to try to keep everything in one place, this could be a great option for you.

Cons: The downside, you may be asked to verify your source of funds. This means you’ll have to have documents saved with you or have access to a person who has it for you. Additionally, there are some reports that their currency exchange rates are not at the current market value.

There are a lot of options for you to consider. Many that are not included in this article due to my research. However, you may disagree with my research. For additional opinions, I highly recommend getting in a few facebook groups and seeking testimonials from fellow digital nomads. The necessary evil of money will not go away. You might as well take care of it the best you can.

Conclusion

To summarize all that we’ve learned today, the biggest lesson I can recommend to you is to read the fine print. I would highly recommend taking the time to consider what you need your financial institution to do for you. Do you need to get paid? Do you need to transfer money? Are you a patient person? As in all scenarios, one size does not fit all. When it comes to money, finding the one that fits will make your digital nomad journey that much more comfortable.

Hope you enjoyed this post on the best bank for digital nomads. Let us know in the comments if you have other suggestions for digital nomad banking solutions!